Personal Finances During COVID-19 Part 1: What You Should and Shouldn’t Do

I’ve taught thousands of people about optimizing their personal finances over the last few years, but this is a more challenging time than usual. In this post, I’ll share a few financial tips specifically for surviving the COVID-19 crisis, and the next post will highlight some of the long-term financial principles you should be thinking about regardless of the global pandemic (A great opportunity if you’re working from home and have extra time!).

Most importantly, remember to ask for help when you need it. In a time of forced isolation, we are all feeling the need for community. If you lost your job or are struggling to pay your rent or buy food, you don’t have to go through this alone – ask those around you for help. If you are still paid while working from home or have enough saved in an emergency fund, consider reaching out to your neighbors and friends who may not be as fortunate and offer to help.

What to do during this crisis:

1. Look at your budget. With extra time on your hands, this is the perfect opportunity to check out your budget and identify ways to save (especially removing monthly subscriptions you don’t use as much as you expected). There are great apps like Mint or Personal Capital that can link to your bank accounts / credit cards and automatically categorize your expenses, allowing you to easily look at trends over the last few months. (You might already be spending less on restaurants, entertainment, and travel during this time…) To make this most effective and keep yourself accountable, grab a friend and compare your monthly expenses.

2. Build up an emergency fund. If you don’t already have an “emergency fund” of six months of expenses, start building it now with what you can save from tip #1. Consider putting your emergency fund in a “high-yield savings account” (interest rates currently around 1.7%) rather than just the normal savings account at your bank.

3. See if you’ll get a tax refund. Even though the government has deferred the tax filing deadline to July 15th, it’s worth using an online platform like TurboTax to quickly fill in your information and estimate your taxes today. If you’re going to get a refund, might as well file now to get the extra cash!

4. Take advantage of student loan changes. If you need the extra cash to help afford essentials, you can pause your student loan payments (and interest) for the next two months with no penalty. Of course, if you can afford to keep making your payments, then continue the journey to being debt-free!

What not to do during this crisis:

1. Don’t take out high-interest loans. Putting additional expenses on a credit card or taking out a payday loan may seem like an easy way to get money quickly, but it will come back to bite you in high interest payments next month, and the next, and the next… Use the tips above first and ask for help from those around you before you dig yourself into a deeper financial hole.

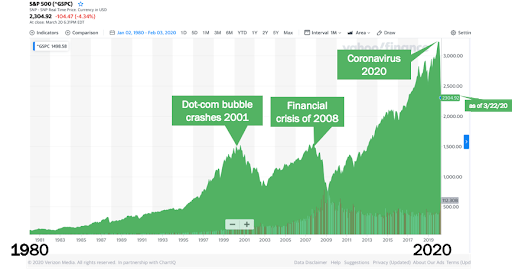

2. Don’t sell assets from your retirement accounts. Unless you are desperate (i.e., you have tried the above tips and still have no way to pay your rent or buy food), now is not the time to panic and sell assets (stocks, mutual funds) from your retirement accounts, assuming retirement is still decades away. When you contribute to your 401(k) or 403(b) or IRA, you are saving for the long term – the market will recover long before you turn 65. Your future self will thank you.

Looking at the S&P 500 over time helps provide the context of where we are today. (Graph from Yahoo Finance)

Posts you may like

-

How to Look Your Best At the 2025 AF Gala

May 7, 2025

-

How Tony Soprano Endorsed Your Mayor

April 29, 2025

-

Renewed Life: An Easter Story

April 18, 2025

-

Start Where You Can This Earth Day

April 17, 2025